A Word of Honest Advice

Before you dive in, know this: the MCA industry is cutthroat. If you jump in solo without relationships, funders will backdoor your deals, steal your merchants, and you'll learn expensive lessons the hard way.

Your best move is to start at a reputable ISO shop or in-house at a funder. Spend time learning the business, understanding how deals actually work, and most importantly — building real relationships with good funders before you try going independent.

Nobody successful in this industry is giving away their playbook online for free. The best way to learn is by positioning yourself near someone who's already winning and making it worth their time to mentor you.

This guide gives you the fundamentals — but experience is the real teacher.

How to Become an MCA Broker in 2026

Everything you need to know about starting a merchant cash advance brokerage in 2026 — from zero experience to funded deals. No fluff, just the practical playbook that working brokers wish they had on day one.

Each step is broken down in detail below.

What Is an MCA Broker?

An MCA broker is the middleman between small business owners who need capital and merchant cash advance funders who supply it. Your job is straightforward: find businesses that need money, match them with the right funder based on their financial profile, submit the deal, and earn a commission when it funds.

Unlike mortgage brokers or insurance agents, MCA brokers do not need years of training, a degree in finance, or (in most states) a license. The barrier to entry is low, which is both the opportunity and the challenge — it means competition is real, but it also means you can go from zero to earning commissions within weeks if you execute properly.

The merchant cash advance industry has grown into a multi-billion dollar market. Small businesses that cannot get approved for traditional bank loans — due to low credit scores, limited time in business, or existing debt — turn to MCAs for fast working capital. As a broker, you are the one who connects that business owner with the right MCA funder for their situation.

A typical day as an MCA broker involves prospecting for new merchants (cold calling, texting, emailing), reviewing bank statements and applications from interested merchants, shopping those deals to your funder panel, following up on submissions, and collecting commissions on funded deals. It is a sales job at its core, and the brokers who treat it like one — with discipline, volume, and consistency — are the ones who make real money.

How MCA Brokers Make Money

MCA broker compensation primarily comes from the spread between the buy rate and sell rate that a funder offers. Understanding how this works is critical because it directly impacts how you structure deals and which funders you prioritize. For a deeper breakdown, read our complete guide to MCA broker commission structures.

Buy Rate / Sell Rate (Points)

When a funder approves a deal, they give you a buy rate (the minimum factor rate they'll accept) and a sell rate (the maximum you can present to the merchant). The difference between the buy and sell rate is your commission — measured in “points.” Typically the spread is around 10 points. On a $75,000 deal with 10 points, you earn $7,500.

You control where you set the rate within that range. If the buy rate is 1.30 and the max sell rate is 1.40, you can present the merchant with anything from 1.30 to 1.40. The higher you sell, the more you make.

Example: $75,000 Deal

Buy Rate

1.30

Sell Rate

1.40

Broker Commission (10 pts)

$7,500

Drop Selling

Sometimes a broker will “drop sell” — meaning they present the merchant with a factor rate lower than the max sell rate to make the deal more attractive. For example, if the sell rate is 1.40 but you offer the merchant 1.35, the deal looks better for them but your commission drops from 10 points to 5 points ($3,750 on a $75K deal). This is a strategic move when competing for a deal or building a long-term relationship with a merchant. You can never sell below the buy rate.

Origination Fees

Most funders charge an origination fee — typically 3-5% — that gets deducted from the funded amount. On a $75,000 advance with a 5% origination fee, the merchant nets $71,250 instead of the full $75,000. Some brokers will drop sell the origination fee (absorb part of it from their commission) to sweeten the deal for the merchant.

Professional Service Fee (PSF)

On top of the funder's commission, brokers can charge the merchant a Professional Service Fee (PSF) — an additional fee for your services in sourcing and structuring the deal. This is disclosed to the merchant and adds to your total earnings per deal. Not every broker charges a PSF, but it's common in the industry.

Renewal Commissions

When a merchant completes their payback and takes a new advance (a “renewal”), many funders pay the original broker a reduced commission — typically 2-5 points. Renewals require almost zero effort from you since the merchant is already a satisfied customer. As your portfolio of funded merchants grows, renewal income becomes a recurring revenue stream that compounds over time. Some experienced brokers earn 30-50% of their monthly income from renewals alone.

Do You Need a License to Be an MCA Broker?

The short answer: no. Because merchant cash advances are structured as purchases of future receivables — not loans — they fall outside traditional lending regulations. You do not need an NMLS number, a lending license, or a Series 7 to broker MCA deals.

The same applies to equipment financing and SBA products — as long as you are working through a funding company that holds the necessary licenses, you as the broker do not need your own. The licensing burden sits with the funder, not the broker.

That said, you should still operate professionally. Get an LLC, use proper contracts with merchants, maintain records, and work with reputable funders. The industry is moving toward more regulation, not less, and brokers who build compliant practices from day one will have an advantage as the landscape shifts.

Setting Up Your MCA Brokerage

You do not need a fancy office or expensive infrastructure to start. Most MCA brokers work from home, especially in the first year. Here is the checklist for getting your business operational:

1. Form Your LLC

Register a limited liability company in your state. This separates your personal assets from business liabilities, gives you credibility when approaching funders, and is required by most funders before they will set you up as an approved broker. Cost: $50-$500 depending on your state. You can file directly with your Secretary of State or use a service like LegalZoom or Northwest Registered Agent.

2. Get Your EIN

Apply for a free Employer Identification Number from the IRS at irs.gov. This takes five minutes and you will need it to open a business bank account and for tax purposes. You receive it instantly online.

3. Open a Business Bank Account

Open a dedicated business checking account. Your commissions will be deposited here, and keeping business finances separate from personal is non-negotiable for tax purposes and professionalism. Most banks offer free or low-cost business checking for new LLCs. Chase, Mercury, and Relay are popular choices.

4. Set Up a Professional Email and Phone

Get a company email (yourname@yourcompany.com) and a dedicated business phone number. Google Workspace costs $7/month and gives you a professional email. For a phone number, services like OpenPhone or Google Voice give you a business line for $15-$25/month. Merchants and funders take you more seriously when you are not calling from a personal Gmail address.

5. Create a Simple Website

You do not need anything elaborate — a one-page site with your company name, what you do, and a contact form is enough. This gives funders something to verify when you apply to broker for them, and gives merchants a place to check your legitimacy. A simple WordPress or Squarespace site costs $10-$20/month.

Startup Cost Breakdown

Building Your Funder Panel

Your funder panel is the roster of MCA companies you can submit deals to. This is arguably the most important asset you build as a broker — the more funders you have, the more deal types you can match, and the more commissions you earn. A weak panel means you are turning away deals that do not fit your limited options.

How Many Funders Do You Need?

Start with 5 to 10 funders that cover the core deal types: first position clean deals, second and third position deals, deals with defaults, low credit score deals, and at least one funder that does reverse consolidations. As you grow, aim for 20-30+ funders to handle any deal that comes across your desk.

Where to Find Funders

The fastest way to build your panel is through the MCA Directory funder search. You can search by the criteria that matter — minimum revenue, credit score, positions, defaults, industry restrictions — and connect directly with ISO reps at each funder. Browse the full merchant cash advance directory to see every funder available.

Other ways to find funders include attending industry conferences (deBanked Broker Fair is the biggest), joining MCA broker communities on Facebook and LinkedIn, and asking other brokers for introductions. Most funders are actively looking for new broker relationships because it means more deal flow for them.

What to Look for in a Funder

Not all funders are created equal. When evaluating a funder for your panel, consider:

- Commission structure: How many points do they pay? Is there room for rate spread? Do they pay renewal commissions?

- Funding speed: How fast do they fund after approval? Same-day funders let you close merchants before they shop around.

- Approval rate: Some funders approve a high percentage of submissions. Others are extremely selective. A mix of both is ideal.

- Deal types: Make sure your panel covers first through fifth+ positions, defaults, low credit, high-risk industries, and different revenue tiers.

- ISO rep responsiveness: If your funder rep takes 24 hours to respond to submissions, you will lose deals. Fast communication is non-negotiable.

- Merchant treatment: Funders who treat your merchants poorly reflect badly on you and kill your renewal pipeline.

Finding Merchants Who Need Funding

Deal sourcing is where most new brokers struggle — and where the separation between successful brokers and ones who quit shows up. You can have the best funder panel in the industry, but if you are not consistently generating merchant conversations, you will not close deals. Here are the primary channels:

Cold Calling

Still the bread and butter for most MCA brokers. You call business owners directly, identify if they have a funding need, and offer to help them get capital. The conversion rate is low (expect 1-3% of calls to result in a submission), but the volume makes it work. A broker making 200-300 calls per day using a power dialer can generate 3-8 interested merchants daily. At that rate, you should be submitting 10-20 deals per week and funding 2-5 of them.

Purchasing Leads

MCA lead vendors sell lists of business owners who have either applied for funding recently, searched for business loans online, or match a financial profile that suggests they need capital. Fresh, exclusive leads cost $15-$50+ each, while aged or shared leads run $2-$10. Browse MCA lead vendors in our marketplace to compare options.

A word of caution: results vary greatly with purchased leads. The space is full of scammy lead providers selling recycled data, outdated lists, or leads that have already been called by 10 other brokers. You might spend $2,000 on a batch and get zero funded deals. Start with a small test before committing serious money, verify the freshness and exclusivity of what you are buying, and ask for references from other brokers who have used the vendor. Finding a reliable lead source is tough and can get expensive — but when you find the right one and dial in your process, the revenue generated is unreal.

Text and Email Campaigns

Many brokers supplement cold calling with SMS campaigns and email marketing. Text messages to business owners have significantly higher open rates than email (90%+ vs 20-30%). However, texting regulations (TCPA) are strict — make sure you are compliant with opt-in requirements and use a reputable platform.

Referral Partnerships

The highest-quality merchants come from referrals. Build relationships with accountants, bookkeepers, business consultants, payment processors, and other professionals who work with small businesses. When their clients need funding, you are the person they call. Referral deals close at 3-5x the rate of cold-called leads and typically have better financials.

Digital Marketing and SEO

Some brokers invest in Google Ads, Facebook Ads, or SEO to generate inbound leads — business owners who come to you already interested in funding. This requires more upfront investment and marketing knowledge, but inbound leads convert at much higher rates. A well-optimized Google Ads campaign for terms like “business cash advance” or “fast business funding” can generate leads at $30-$75 each.

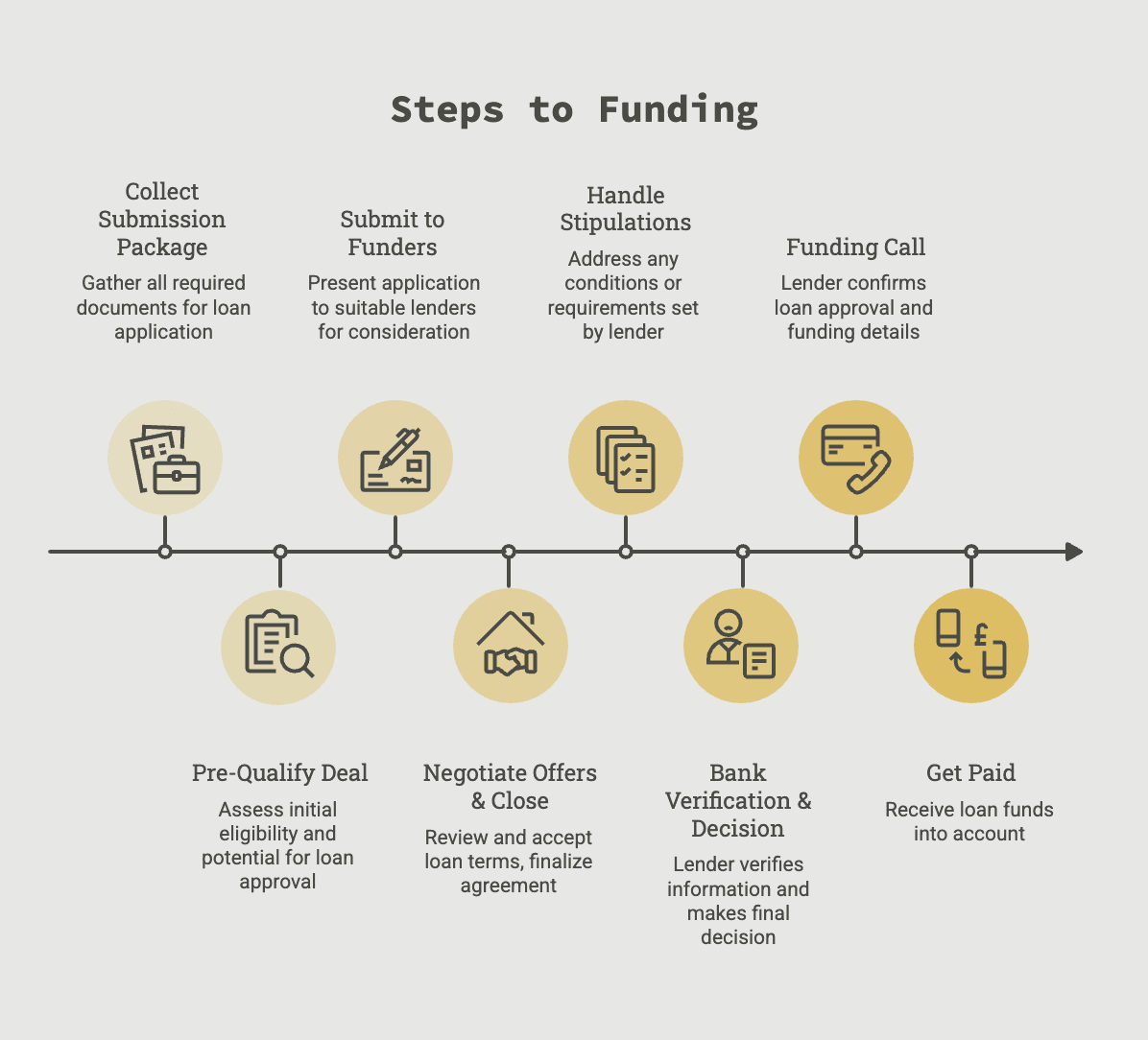

Submitting Your First Deal

You have a merchant who needs funding. Now what? The submission process is standardized across most funders, and speed matters — the faster you get a complete package to funders, the faster the merchant gets funded and you get paid.

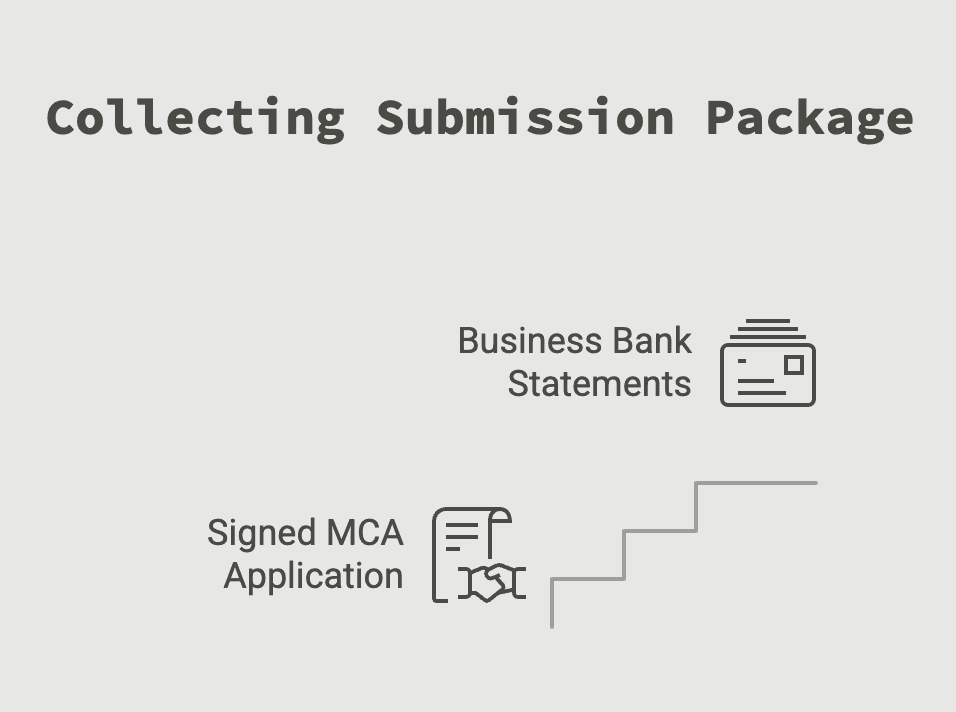

Step 1: Collect the Submission Package

Every funder needs the same core documents:

- Signed MCA application: Most funders have their own application, but many accept a universal broker application. Get the merchant to fill out basic business information, owner details, and funding request amount.

- 3-4 months of business bank statements: This is the most important document. Funders underwrite primarily on cash flow — monthly deposits, average daily balance, negative days, and NSF (non-sufficient funds) activity. All pages of each statement are required.

- Valid government-issued ID: A copy of the business owner's driver's license or passport.

- Voided check: From the business bank account where the advance will be deposited and ACH payments will be debited.

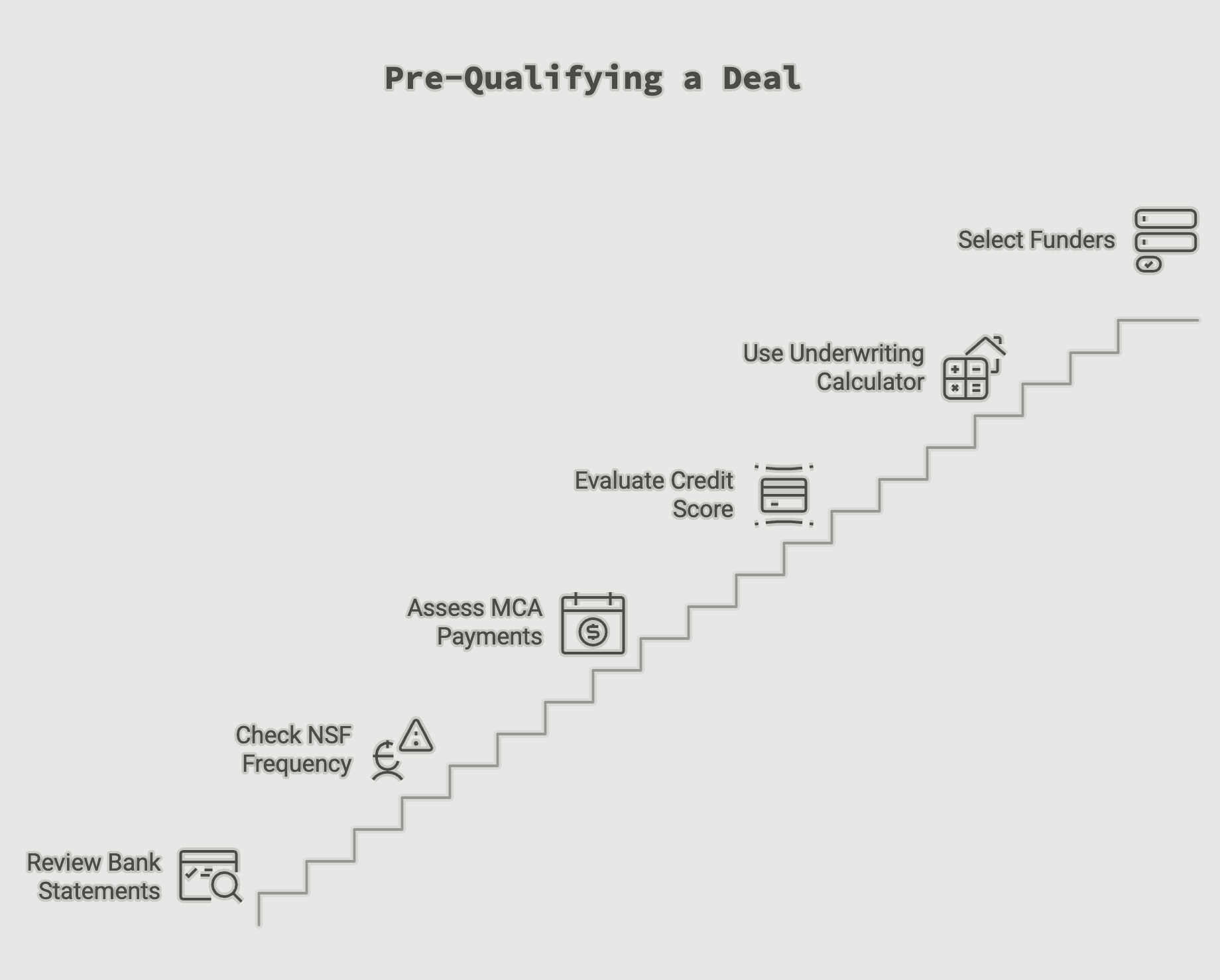

Step 2: Pre-Qualify the Deal

Before blasting the deal to every funder on your panel, take 10 minutes to review the bank statements yourself. Use the underwriting calculator to model the deal. Look at monthly revenue (total deposits minus transfers), average daily balance, NSF frequency, existing MCA payments (daily ACH debits to known funders), and the owner's credit score. This tells you which funders to submit to and saves you from wasting time on deals that will not fund.

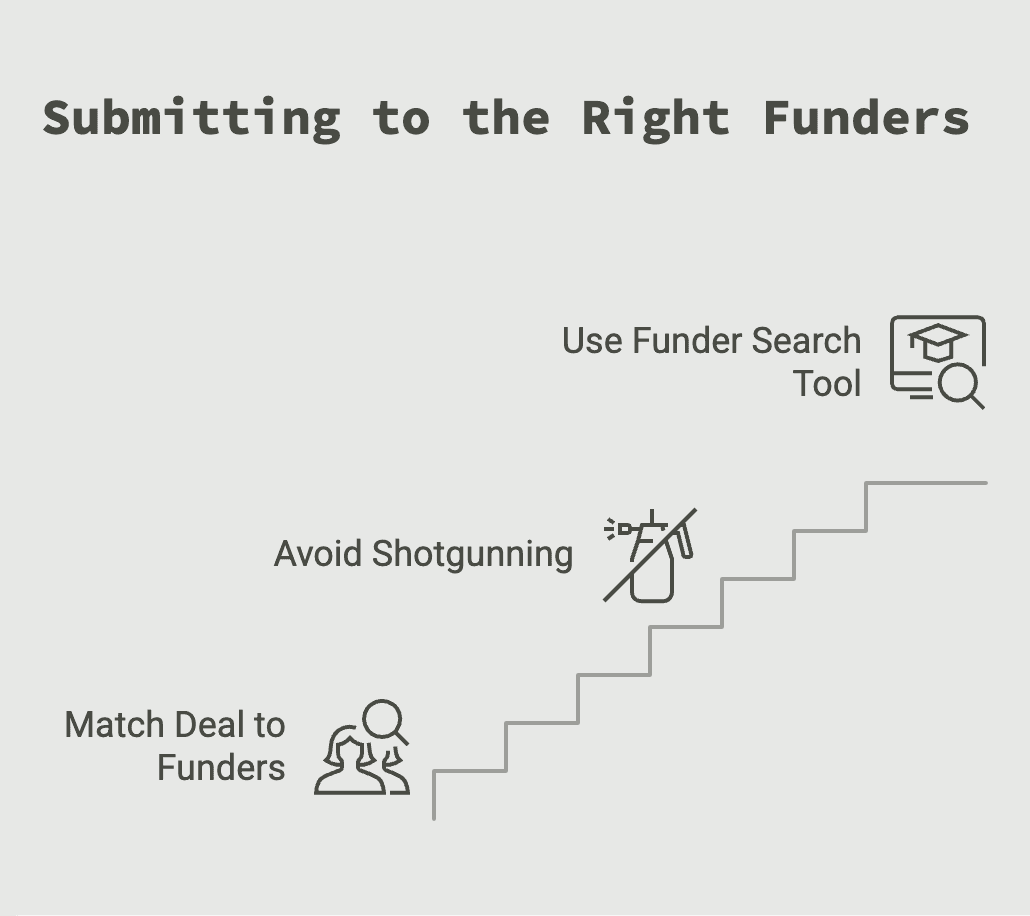

Step 3: Submit to the Right Funders

Match the deal to 3-5 funders from your panel based on the merchant's profile. Submitting to too many funders simultaneously (“shotgunning”) can actually hurt you — funders see each other's credit pulls, and excessive submissions signal desperation. Use the funder search tool to identify the best matches by revenue, credit score, and position count.

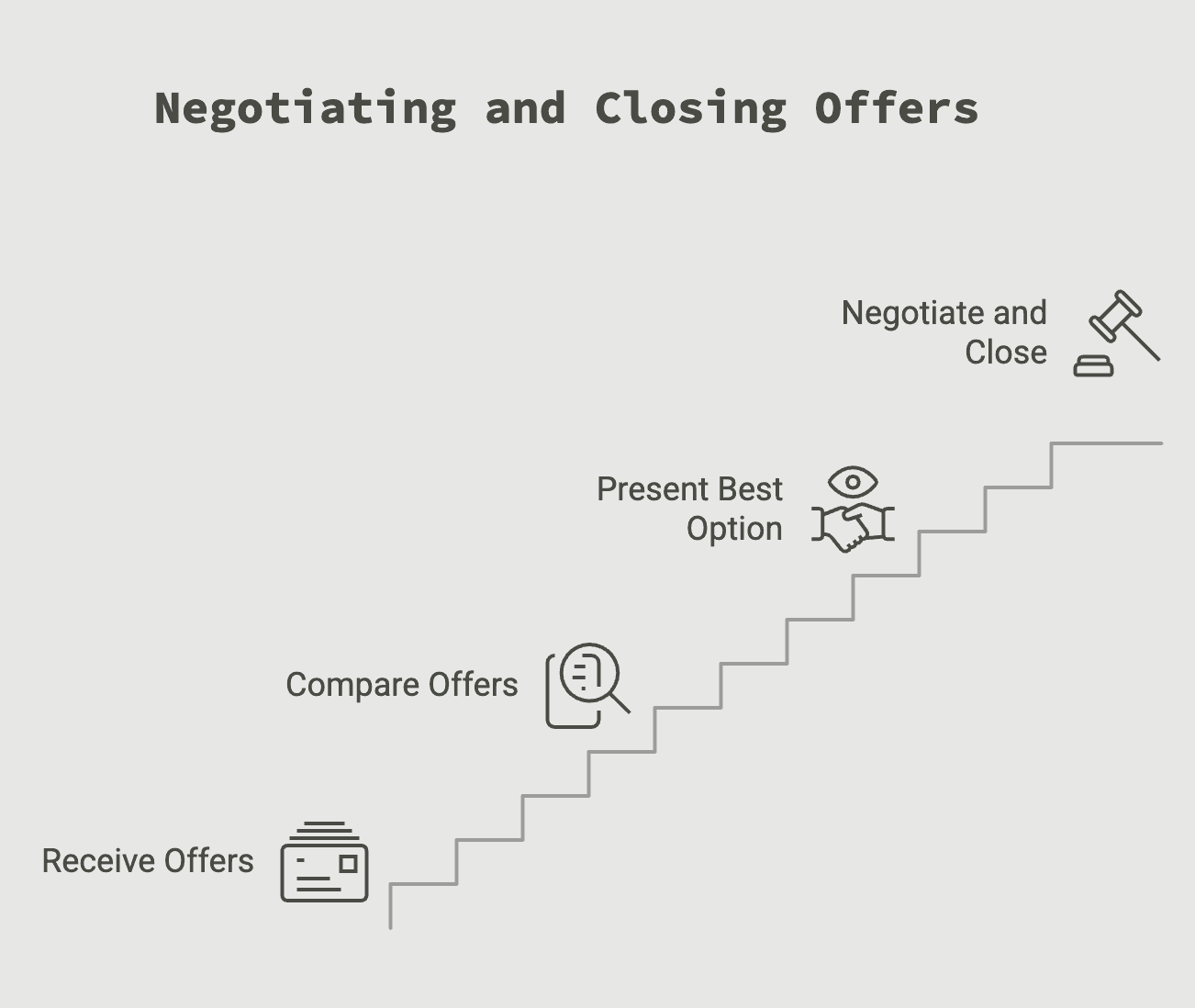

Step 4: Negotiate Offers and Close

Once you receive offers from funders (usually within 1-4 hours for clean deals), compare them on total funding amount, factor rate, payback period, and daily/weekly payment amount. Present the best option to the merchant.

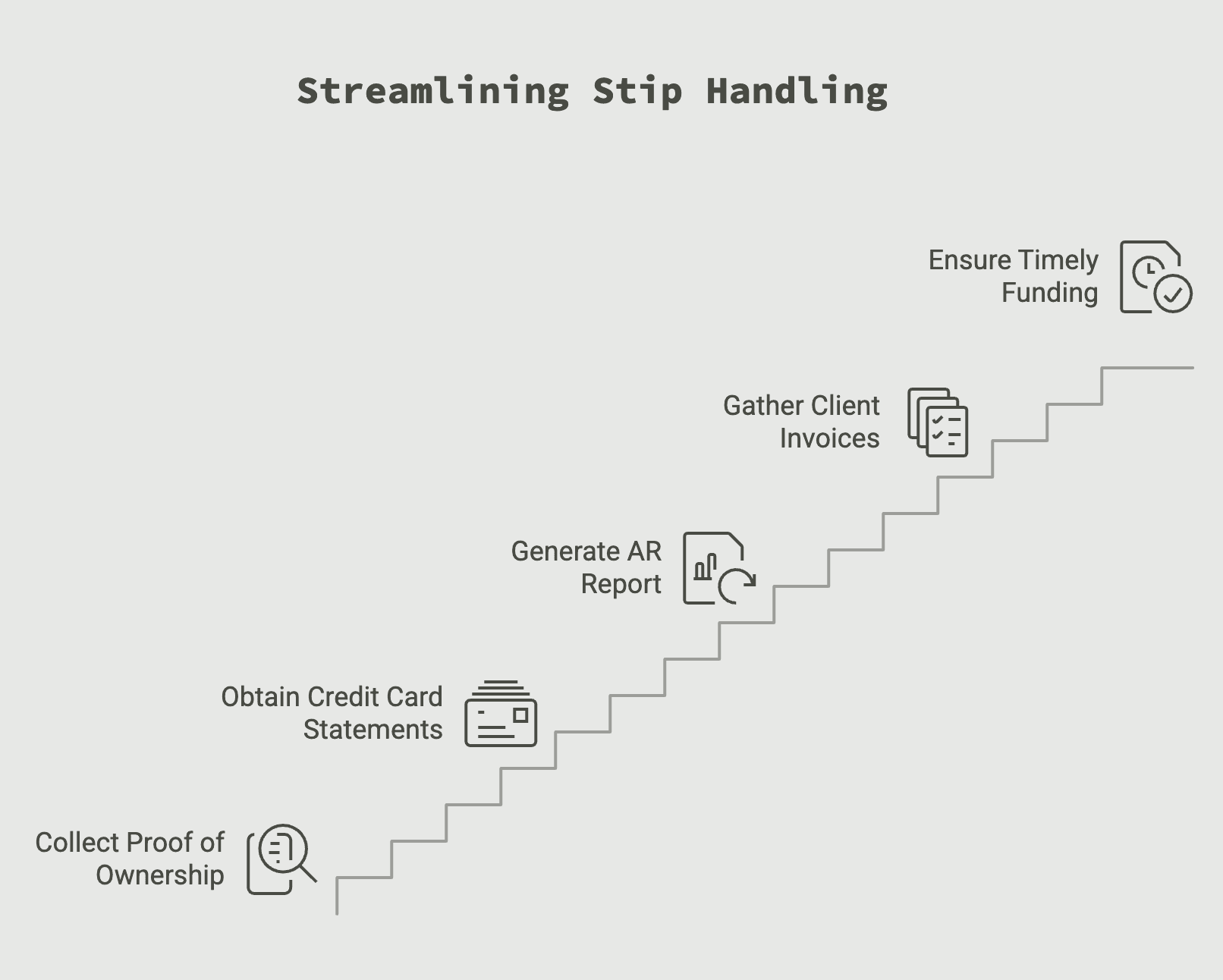

Step 5: Handle Stipulations

After the merchant accepts an offer, most funders will come back with “stips” — additional documents they need before they can fund. Common stipulations include:

- Proof of ownership: EIN letter from the IRS, K-1 report, or business tax returns to verify the applicant actually owns the business.

- Credit card processing statements: If the business accepts credit cards, funders may ask for the most recent month's processing statement to verify volume.

- Accounts receivable (AR) report: For B2B businesses, funders want to see outstanding invoices and client payment history.

- Client invoices: Some funders request copies of active invoices to verify revenue sources.

How fast you collect stips from the merchant directly impacts how fast the deal funds. Stay on top of the merchant — most deals die because the broker let the merchant go silent during the stip phase.

Step 6: Bank Verification and Decision Logic

Before funding, the funder will verify the merchant's bank account in real time. This is done either through a manual bank login (where the funder logs into the merchant's online banking with permission) or through a service like Decision Logic or Plaid. They are confirming three things: the current balance is healthy, there is no suspicious activity, and there are no signs of double funding — meaning the merchant hasn't taken another advance between the time they applied and the time of funding.

Step 7: Funding Call

Once stips and bank verification clear, the funder conducts a funding call. This is a 10-minute call between the funder and the merchant where the funder goes over the terms of the agreement — advance amount, factor rate, total payback, daily/weekly payment amount, and the merchant's obligations. The funder also conducts a brief merchant interview to confirm business details and verify the owner is who they say they are. This call is recorded for compliance.

Step 8: Get Paid

After the funding call clears, the funder sends a “funded email” to the broker confirming the deal details — advance amount, factor rate, payback, and your commission breakdown. Your commission is typically wired or ACH'd to your business account within 1-3 business days of the deal funding. Some funders pay same day, others can take up to 10 days. Track every submission and funded deal in your CRM so nothing slips through the cracks.

Step 9: Clawbacks and the ISO Agreement

Most funders have a 30-day clawback policy — if the deal goes bad within 30 days of funding (the merchant defaults, stops making payments, or closes their account), the funder will claw back your commission. This means you have to return the money. This is standard across the industry and is outlined in your ISO agreement — the contract between you (the broker) and the funder that governs your relationship.

The ISO agreement is a trust-based arrangement. The funder trusts that you will return the clawback commission if a deal goes bad. The broker trusts that the funder will pay commissions on time and in full. If a funder consistently delays or fails to pay commissions, stop sending them deals — there are plenty of funders who pay reliably. On the flip side, if a broker refuses to pay back a clawback, the funder will cut that broker off permanently and word spreads fast in this industry.

Before you start submitting deals to any funder, read their ISO agreement carefully. Pay attention to commission payout timelines, clawback terms, renewal protection, and exclusivity clauses.

Tools Every MCA Broker Needs

The right tools multiply your output. A broker with a dialer and CRM will close more deals in a week than a broker making manual calls and tracking leads in a notebook will close in a month. Here is the essential tech stack:

CRM Software

Track every lead, follow-up, submission, and funded deal. Without a CRM, you will forget to follow up with merchants, lose track of submissions, and leave money on the table. MCA-specific CRMs like Industrio and ISOAmp include features for tracking submissions across multiple funders.

Browse CRM Options →Power Dialer

Cold calling 200+ numbers a day manually is impossible. A power dialer automates the process — it dials the next number as soon as you finish a call, skips voicemails, and lets you leave pre-recorded messages. This 5-10x your daily call volume compared to manual dialing.

Browse Dialer Options →SMS / Texting Platform

Text campaigns reach business owners where they pay attention. A dedicated MCA texting platform handles compliance, opt-outs, and lets you send at scale. Response rates on texts are dramatically higher than email for initial merchant outreach.

Browse Texting Options →Email Marketing

Email campaigns for lead nurturing and drip sequences. Once a merchant shows interest but is not ready to apply yet, automated email follow-ups keep you top of mind for when they are ready. Also useful for re-engaging past funded merchants for renewals.

Browse Email Tools →Underwriting Calculator

Before you submit a deal, model it. Plug in the advance amount, factor rate, and term to see total payback, daily payment amount, and effective cost. This helps you pre-qualify deals and present clear numbers to merchants.

Use the Calculator →Funder Directory

Quickly find which funders match a specific deal by searching criteria like revenue, credit score, positions, and industry. Saves you from submitting to funders who will reject the deal and helps you discover new funders for niche deal types.

Search the Directory →Common Mistakes New MCA Brokers Make

The MCA industry has a high turnover rate among new brokers — most quit within the first 3 months. It is not because the opportunity is not real. It is because they make avoidable mistakes that kill their momentum before they get traction. We wrote a detailed breakdown of the most common mistakes, but here are the highlights:

1. Inconsistent Prospecting

The number one killer of new MCA brokerages is inconsistent outreach. Brokers make calls for two days, get no immediate results, and take a day off. That day becomes three days, then a week. This business requires daily, sustained outreach — 200+ calls, 100+ texts, or equivalent marketing activity every single day. The brokers who fund 10+ deals a month never stop prospecting, even when they have deals in the pipeline.

2. Too Few Funders on Their Panel

New brokers often start with 2-3 funders and wonder why they cannot fund deals. A merchant who does not qualify with Funder A might be a perfect fit for Funder B. Every deal you cannot place because you do not have the right funder is money left on the table. Build your panel to at least 10 funders in your first month, covering different risk profiles and deal types.

3. Not Reviewing Bank Statements Before Submitting

Submitting garbage deals to funders — merchants with $5,000 in monthly revenue, daily negative balances, or obvious fraud signals — damages your reputation with funders. After enough bad submissions, funders start deprioritizing your deals or dropping you entirely. Spend 10 minutes reviewing bank statements before you submit anything. Learn the key underwriting terms funders care about.

4. Overpromising to Merchants

Telling a merchant they will get $200,000 when their bank statements support $40,000 destroys trust and kills the deal. Be realistic about what a merchant qualifies for based on their financials. Under-promising and over-delivering is always better — a merchant who expected $30,000 and got approved for $50,000 becomes a loyal repeat customer.

5. Ignoring Renewals

New brokers focus exclusively on new merchant acquisition and forget about the goldmine sitting in their funded portfolio. Set a reminder to follow up with every funded merchant when they reach 50-60% payback on their advance. Renewal deals fund faster, close easier, and still pay commissions. This is the path to predictable monthly income.

6. Going It Completely Alone

The MCA industry runs on relationships and shared knowledge. Join broker communities, attend industry events, and connect with other brokers. You will learn about new funders, get tips on deal structuring, hear about lead sources that work, and avoid scams. Nobody succeeds in this business in isolation.

How Much Money Can You Make as an MCA Broker?

MCA brokering has uncapped earning potential, which is part of the appeal. But let us be realistic about what different experience levels actually earn. These numbers are based on industry averages — your results depend entirely on your effort, deal quality, and funder relationships.

Months 1-3 (New Broker)

$0 - $10K/mo

Most new brokers fund their first deal in weeks 3-6. Early months are heavy on learning, building your funder panel, and figuring out your prospecting rhythm.

Typical: 1-3 funded deals/month

Avg deal size: $25,000 - $50,000

Commission: $2,500 - $7,500 per deal

Months 6-12 (Intermediate)

$10K - $30K/mo

By month 6, you have a working funder panel, a refined prospecting system, and early renewals starting to come in. Your deal-closing efficiency improves significantly.

Typical: 5-10 funded deals/month

Avg deal size: $40,000 - $75,000

Commission: $4,000 - $10,000 per deal

Year 2+ (Experienced)

$30K - $100K+/mo

Experienced brokers with strong funder relationships, a large renewal portfolio, and possibly a small team can earn six figures monthly. Renewal income alone can reach $15,000-$30,000/month.

Typical: 15-30+ funded deals/month

Avg deal size: $50,000 - $150,000

Commission: $5,000 - $20,000+ per deal

The math is simple: if you fund 8 deals per month at an average of $50,000 each and earn 10 points per deal, that is $40,000/month in commission. Add rate spread and renewals, and you can see how top brokers reach $50,000-$100,000+ monthly. But reaching that level requires 12-24 months of consistent effort and volume.

Be honest with yourself: months 1-3 will be the hardest. Many new brokers earn nothing in their first month. If you cannot afford to go 4-8 weeks without income, keep your day job and start part-time. The opportunity is real, but it is not instant.

Frequently Asked Questions

Do you need a license to become an MCA broker?

How much money do you need to start an MCA brokerage?

How much do MCA brokers make per deal?

How long does it take to close your first MCA deal?

Do I need prior finance experience to become an MCA broker?

What is the difference between an MCA broker and an ISO?

Can you be an MCA broker part-time?

What documents do funders need to underwrite an MCA deal?

How do I find funders to work with as a new broker?

What is the best CRM for MCA brokers?

Ready to Start Brokering MCA Deals?

Search MCA funders by deal criteria, connect with ISO reps, and start building your funder panel today. Creating an account is free and takes 30 seconds.